Transparency Drives Investor Satisfaction, Yet Investment Firms Aren’t Proactively Explaining Fees In Canada

Edward Jones Ranks Highest among Full Service Investment Firms in Canada for a Third Consecutive Year

TORONTO: 20 August 2015 — Despite the recent CRM2[1] regulatory mandate requiring increased transparency around investment fees and performance, investment firms have generally been slow or ineffective in ensuring advisors are proactively explaining fees and performance to their clients, missing a critical opportunity to build trust and loyalty, according to the J.D. Power 2015 Canadian Full Service Investor Satisfaction StudySM released today.

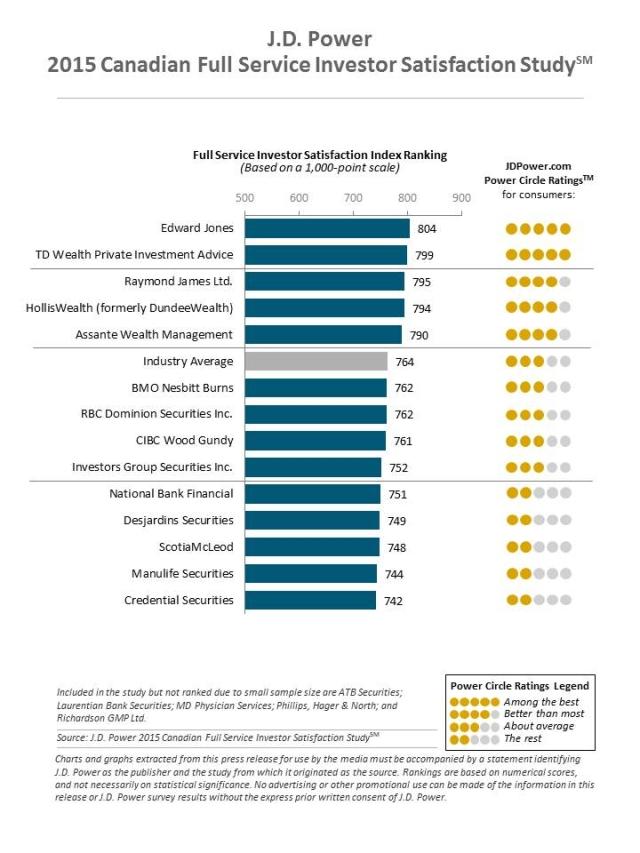

The study provides benchmarks of satisfaction that allow individual investment firms in Canada to compare their performance with other firms included in the study. Overall investor satisfaction with full service investment firms and financial institutions that offer wealth management and private banking services is measured in seven factors (in order of importance): investment advisor (39%); investment performance (18%); account information (17%); product offerings (14%); commissions and fees (8%); website (3%); and problem resolution (1%). Overall satisfaction is 764 (on a 1,000-point scale), up by 9 points from 2014.

Transparency for investors around fees and account performance remains a big challenge for the wealth management industry. Three in four (75%) investors do not completely understand the commissions and fees they pay their firm, and 45 percent indicate their firm hasn’t provided them with a summary of fees and commissions charged. In terms of advisor guidance, 43 percent of investors do not receive an explanation of the firm’s fee structure and 33 percent do not receive an explanation of their investment performance.

“Firms are increasingly required to provide investors with greater transparency on both fees and performance. Advisors should view this as an opportunity to deepen their relationship with clients by having discussions that provide appropriate context,” said Mike Foy, director of the wealth management practice at J.D. Power. “For example, advisors need to make sure investors understand the value of what they’re getting for what they pay, and advisors also need to evaluate portfolio performance relative to staying on track toward achieving personal goals instead of trying to beat the market. This approach provides a much more satisfying client experience than when an investor simply receives a mandated transparency report with details that don’t provide any meaningful explanations.”

According to the study, transparency increases satisfaction, especially when advisors take the time to explain the fees. Satisfaction increases by 62 points, on average, when firms provide a summary of fees, compared to when they don’t (792 vs. 730, respectively), and improves by 87 points when advisors provide an explanation of fees, compared to when they don’t (801 vs. 714). Satisfaction is higher among fee-based investors than among commission-based investors (784 vs. 764, respectively). Additionally, fee-based investors tend to be less negatively impacted by mandated disclosures, since commission-based accounts often include embedded fees paid by the mutual fund companies that investors may not know about.

KEY FINDINGS

- Providing an outstanding overall investor experience generates high levels of retention, advocacy and referrals—all critical drivers of new business. The study finds that 76 percent of highly satisfied investors (overall satisfaction scores of 900 or higher) say they “definitely will” recommend their firm; 72 percent say they “definitely will not” switch firms; and 28 percent say they “intend to increase” the amount invested with their primary firm.

- Investment advisor satisfaction is lowest among younger investors (Gen Y/Z[2]) at 768 and highest among older investors (Pre-Boomers, Boomers and Gen X) at 835, suggesting firms need to better understand and adapt to the needs and priorities of Gen Y/Z investors as these segments grow.

- Gen Y/Z investors have significantly different expectations and preferences in how they work with an advisor compared with all other generational groups. Four in 10 (42%) full service investors in Gen Y/Z consider themselves “validators,” or those who like to actively come up with their own investment ideas and use an advisor as a sounding board; 49 percent say they are “collaborators,” those who collaborate with an advisor and depend on their guidance and advice; and 10 percent are “delegators”—those who prefer to depend on their advisor to make decisions on their behalf. Among Pre-Boomers, Boomers and Gen X investors, just 26 percent, in aggregate, consider themselves “validators”; 63 percent “collaborators”; and 11 percent “delegators.”

- Advisors are missing an opportunity to connect with investors about the needs of their next-generation beneficiaries. Gen Y/Z investors will continue to increase in importance as the enormous intergenerational transfer of wealth occurs over the coming decades. Just 29 percent of investors say their advisor has asked about the needs of their beneficiaries, with satisfaction 40 points higher among those whose advisors have asked.

Investment Firm Rankings

Edward Jones ranks highest in investor satisfaction with full service investment firms in Canada for a third consecutive year, with a score of 804, which is a 13-point increase from 2014. Edward Jones performs particularly well in three factors: investment advisor; investment performance; and product offerings. Following in the rankings are TD Wealth Private Investment Advice and Raymond James Ltd. (799 and 795, respectively).

The 2015 Canadian Full Service Investor Satisfaction Study is based on responses from 4,827 investors who use advice-based investment services from financial institutions in Canada. The study was fielded in May and June 2015.

Media Relations Contacts

Gal Wilder; Cohn & Wolfe; Toronto, Canada; 647-259-3261; gal.wilder@cohnwolfe.ca

Beth Daniher; Cohn & Wolfe; Toronto, Canada; 647-259-3279; beth.daniher@cohnwolfe.ca

John Tews; J.D. Power; Troy, Mich; 248-312-4119; media.relations@jdpa.com

About J.D. Power and Advertising/Promotional Rules www.jdpower.com/about-us/press-release-info

About McGraw Hill Financial www.mhfi.com

[1] For information about The Client Relationship Model - Phase 2 (CRM2), go to: https://www.osc.gov.on.ca/en/Dealers_crm2-faq-planning-tips.htm

[2] J.D. Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2004). For purposes of this analysis, Gen Y and Gen Z are combined, as respondents are required to be at least 18 years old to participate in the study.