Canada’s Banks Lose Appeal with Younger Customers, J.D. Power Finds

TD Canada Trust (Large Banks) and Tangerine (Midsize Banks) Top the Ranks in Customer Satisfaction

TORONTO: 2 May 2019 – While overall customer satisfaction with Canada’s large and midsize banks increases slightly this year, the banks are losing some appeal with customers under the age of 40, according to the J.D. Power 2019 Canada Retail Banking Satisfaction Study,SM released today.

Overall satisfaction with Canada’s retail banks increases to 785 from 782 (on a 1,000-point scale) in 2019. However, satisfaction among customers under age 40 declines to 777 from 780, while satisfaction among customers age 40 and older increases to 792 from 785. A five-point satisfaction difference between the two age segments in 2018 has grown to a 15-point difference in 2019.

The decline among customers under age 40 spans every factor, with the biggest declines in: in-person bank branch service (-14); problem resolution (-13 points); automated phone service (-13); live phone service (-10); and assisted online service (-10). Satisfaction declines are smaller in automatic banking machines, online and mobile banking service.

The study shows that the number of digital-centric1 retail banking customers increases 6 percentage points, while the number of branch-dependent customers declines 6 percentage points. While customers are expanding their use of digital banking services and use branches less often, these customers experienced service quality declines during problem resolution, branch and telephone interactions.

“The findings highlight a key battleground for banks,” said Paul McAdam, Senior Director of Banking Intelligence at J.D. Power. “Younger and digital-centric customers are vital to future business growth, but younger customers are more likely to receive inconsistent service levels. Banks have invested heavily in convenience, in digitizing transactions and in making products easier to use. Service quality, however, is not keeping pace in omni-channel interactions. Banks that don’t address the gaps in service expectations are at an increased risk of client departures.”

According to the study, younger customers are three times more likely to switch banks than older customers. During the past year, 9% of bank customers under the age of 40 say they have switched banks, compared with 3% of those age 40 and older.

Following are additional key findings of the 2019 study:

- Products and fees deliver: Year over year, overall customer satisfaction with bank products and fees has increased significantly, driven by improved satisfaction with the reasonableness of fees and the competitiveness of interest rates on chequing and savings accounts. Customers cite reduced incidences of paying fees, and customer understanding of bank fee structures improves from 2018.

- Frequent communication appreciation: Another category showing an increase in satisfaction is communication and advice. Communications improves between banks and their customers—especially in terms of relevancy and frequency.

- Problem resolution is…problematic: The incidence of customer problems declines slightly, but satisfaction with bank problem resolution also declines due to lower ratings for the ease of getting problems resolved and with the knowledge of bank representatives involved in problem resolution.

- Telephone service declines: Satisfaction with live representative telephone service declines due to lower ratings for the speed of completing transactions and the knowledge of phone representatives. Customers also cite higher incidences of being placed on hold as well as lower incidences of phone reps providing their name and greeting customers by name.

Study Rankings

The study measures customer satisfaction with Canada’s large and midsize banks. The scores reflect satisfaction of the entire retail banking customer pool of these banks, representing a broader group of customers than in just the branch-dependent and digital-centric segments.

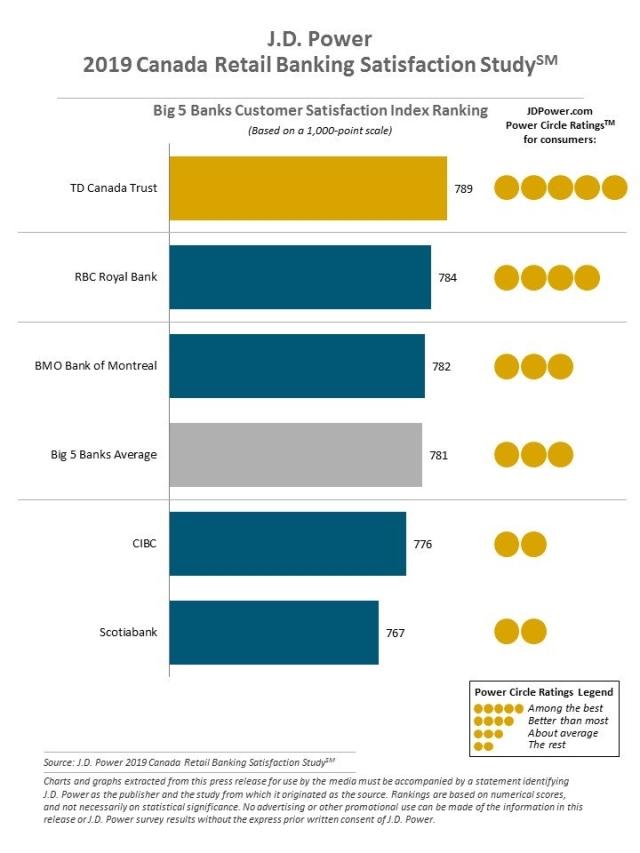

Among the Big 5 banks, TD Canada Trust ranks highest with a score of 789. RBC Royal Bank (784) ranks second and BMO Bank of Montreal (782) ranks third.

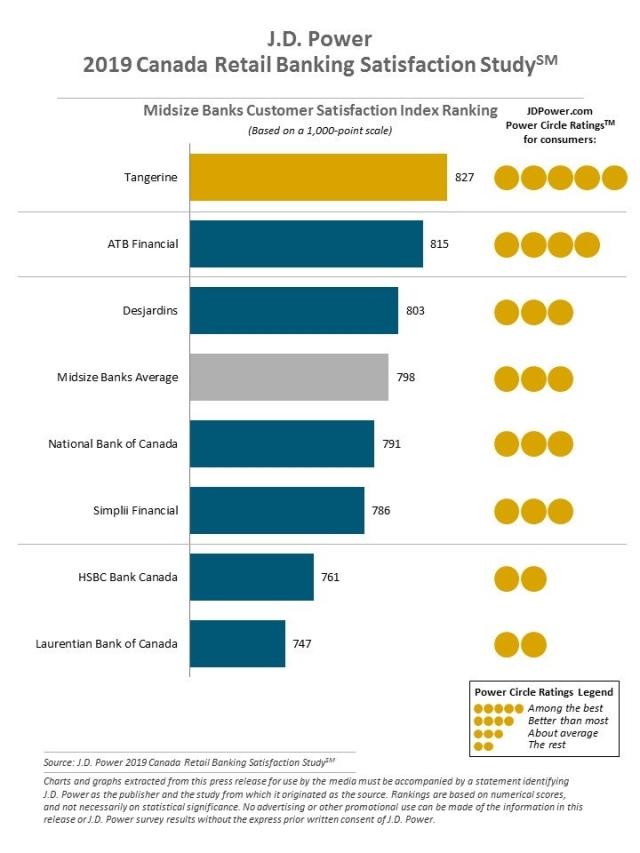

Among midsize banks, Tangerine ranks highest for an eighth consecutive year, with a score of 827. ATB Financial (815) ranks second and Desjardins (803) ranks third.

The Canada Retail Banking Satisfaction Study measures customers’ satisfaction in six factors (listed in alphabetical order): channel activities; communication/advice; convenience; new account opening; problem resolution; and products/fees. Channel activities include seven sub-factors (listed in alphabetical order): assisted online service; ABM; branch service; call centre service; IVR/automated phone service; mobile banking; and online banking. The study is based on responses from more than 15,000 retail banking customers of Canada’s largest and midsize banks regarding their experiences with their retail bank. It was fielded in two waves from June 2018 through January 2019.

For more information about the Canada Retail Banking Satisfaction Study, visit https://canada.jdpower.com/resource/canada-retail-banking-satisfaction-study.

J.D. Power is a global leader in consumer insights, advisory services and data and analytics. These capabilities enable J.D. Power to help its clients drive customer satisfaction, growth and profitability. Established in 1968, J.D. Power has offices serving North America, South America, Asia Pacific and Europe.

Media Relations Contacts

Gal Wilder, Cohn & Wolfe; 647-259-3261; gal.wilder@cohnwolfe.ca

Sandy Caetano, Cohn & Wolfe; 647-259-3288: sandy.caetano@cohnwolfe.ca

Geno Effler, J.D. Power; Costa Mesa, Calif.; 714-621-6224; media.relations@jdpa.com

About J.D. Power and Advertising/Promotional Rules: http://www.jdpower.com/business/about-us/press-release-info

1Digital-centric customers use the online and mobile banking services of their banks but have used branch offices no more than once in the past three months. Branch-dependent customers have used branches two or more times in the past three months and may or may not have used online and mobile banking services.