Good Service Trumps Low Pricing in Canada’s Competitive Auto Lending Marketplace

BMW Financial Services Ranks Highest in Dealer Satisfaction in the Prime Retail Credit Segment;

VW Credit Canada Ranks Highest in Floor Planning

TORONTO: 1 June 2015 —For new-vehicle dealerships in Canada, receiving good service and fast contract funding for all consumer-facing products—prime retail credit, non-prime retail credit and retail leasing—is more important than obtaining low pricing offered by auto finance providers, according to the J.D. Power 2015 Canadian Dealer Financing Satisfaction StudySM released today.

The study, now in its 17th year, measures dealer satisfaction with finance providers in four segments: prime retail credit; retail leasing; floor planning; and non-prime retail credit.[1] Satisfaction is calculated on a 1,000-point scale. Dealer satisfaction in the prime retail credit segment is 850, and in the non-prime retail credit segment satisfaction is 848. Dealer satisfaction in the retail leasing segment is 853, while in the floor planning segment, satisfaction is 934.

New-vehicle dealers prefer personalized service from their underwriting funding and sales teams that expedites consumer applications and funds contracts over obtaining lower pricing from their finance provider. Approximately one-third (32%) of dealers are willing to pay a roughly 0.70-basis-point premium, on average, for access to an enhanced service and financing experience. Dealers want a central point of contact in underwriting, whether an individual or team; yet, 37 percent of prime retail credit dealers do not have any dedicated support.

Dealer-focused sales rep relationships increase satisfaction and retail contract volume. When a high level of sales rep service is provided, satisfaction is substantially higher than when there is no focused support (943 vs. 744, respectively). Among dealers with a focused relationship where all sales rep relationship key performance indicators (KPIs) are met, 67 percent say they “definitely will” increase the percentage of business they conduct with their provider.

“High-performing lenders are characterized as collaborative consultants rather than loan processors,” said Mike Buckingham, senior director of the automotive finance practice at J.D. Power. “What separates the highest-performing lenders from the rest is the broad range of support they provide dealers to help sell vehicles. This includes helping dealers understand the variety of lending options available, how to maximize profits, how to reduce expenses and how to effectively retain customers. Dealers, in many instances, are willing to pay a premium price to receive these services from the high-performing lenders.”

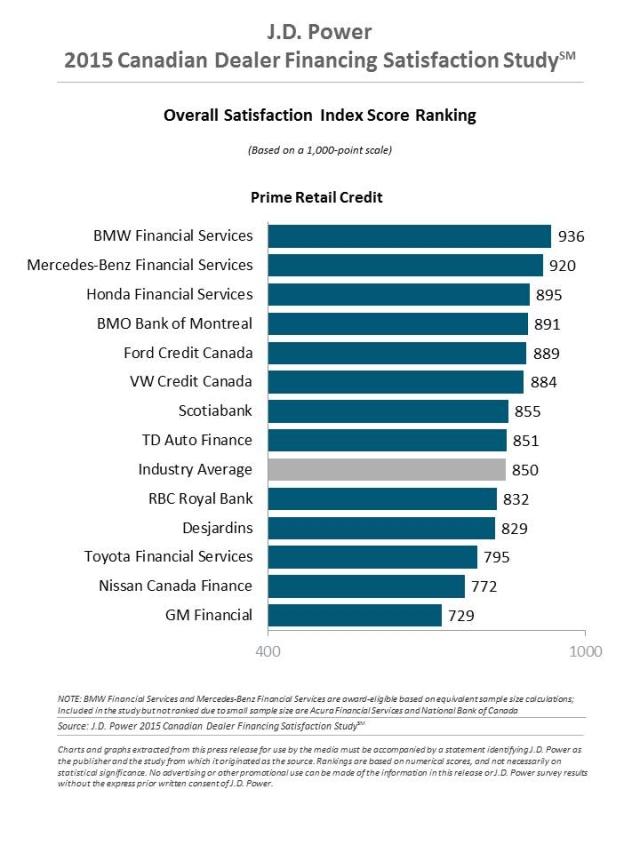

Prime Retail Credit Segment Rankings

BMW Financial Services ranks highest in the prime retail credit segment with a score of 936 and performs particularly well across all factors. Mercedes-Benz Financial Services ranks second in the segment with a score of 920, followed by Honda Financial Services at 895.

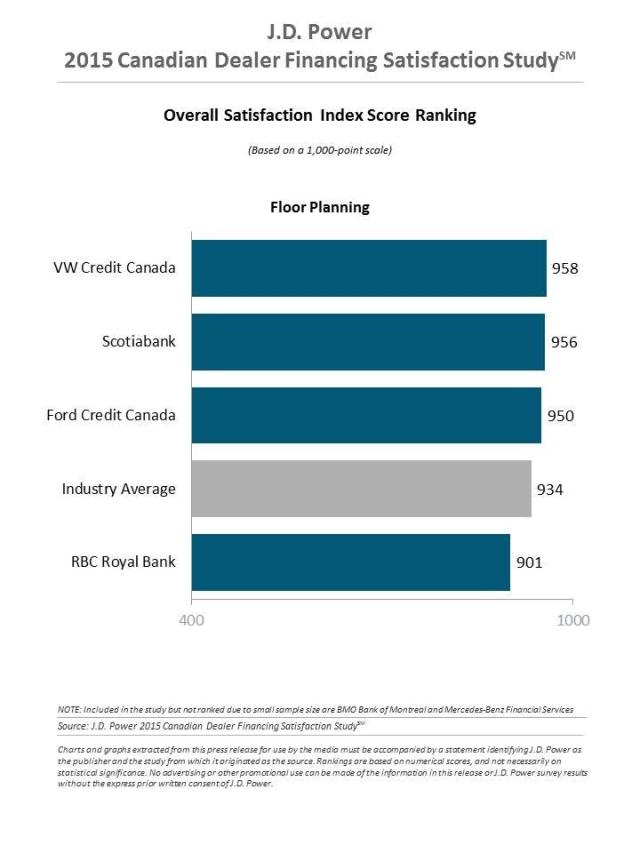

Floor Planning Segment Rankings

VW Credit Canada ranks highest in the floor planning segment with a score of 958 and performs well across all factors. Scotiabank (956) ranks second and Ford Credit Canada (950) third.

Retail Leasing and Non-Prime Retail Segments

While there are no awards presented in the retail leasing and non-prime retail segments, BMW Financial Services, Honda Financial Services and VW Credit Canada perform particularly well in the retail leasing segment; and Ford Credit Canada and Scotia Dealer Advantage perform above the non-prime retail segment average.

KEY FINDINGS

- Dealers are interested in building a collaborative relationship with their lenders. When lenders provide primary buyer/underwriter personnel to facilitate credit approvals and speedy contract funding in the application and approval process, satisfaction increases significantly in the prime retail credit segment (+81 points) and non-prime retail credit segment (+76).

- In the finance provider offering factor for the prime retail credit segment, flexibility with the buying policy (17%) is the most important attribute, compared with competitiveness of rates with new vehicles (14%) and used vehicles (11%).

- When the lenders’ sales representative visits the dealership a minimum of five times per year, satisfaction increases in prime retail credit (+90 points), in non-prime retail credit (+94) and in floor planning (+45). In retail leasing, satisfaction increases by 89 points with just four visits per year.

- In retail leasing, paperwork is a tremendous burden to the dealer in the lease return process, as 68 percent of leases are returned to the dealership. Nearly two-thirds (65%) of dealers experience challenges with this process. When finance providers guide customers through the lease return process—easing dealer burden—satisfaction is positively impacted by 126 points.

Satisfaction is measured across three factors in the prime and non-prime retail credit segments: finance provider offerings; application and approval process; and sales representative relationship. Four factors are measured in the retail leasing segment: finance provider offerings; application and approval process; sales representative relationship; and vehicle return process. Four factors are measured in the floor planning segment: finance provider credit line; floor plan support; sales representative relationship; and floor plan portfolio management.

The 2015 Canadian Dealer Financing Satisfaction Study captures nearly 6,300 finance provider evaluations across the four segments. These evaluations were provided by roughly 1,300 new-vehicle dealerships in Canada. The study was fielded between January and March 2015.

Media Relations Contacts

Gal Wilder; Cohn & Wolfe; Toronto, Ontario; 416-924-5700; gal.wilder@cohnwolfe.ca

Beth Daniher; Cohn & Wolfe; Toronto, Ontario 647-259-3290; beth.daniher@cohnwolfe.ca

John Tews; J.D. Power; Troy, Mich. 248-680-6218; media.relations@jdpa.com

About J.D. Power and Advertising/Promotional Rules http://www.jdpower.com/about-us/press-release-info About McGraw Hill Financial www.mhfi.com

[1]No awards are presented in the retail leasing and non-prime retail credit segments due to insufficient market representation of the respective segments in the 2015 study.