Canadian Banks Face Untimely Digital Banking Headwinds Since Pandemic Began, J.D. Power Finds

RBC Royal Bank (Big 5 Banks) and Tangerine (Midsize Banks) Rank Highest in Customer Satisfaction

TORONTO: 7 May 2020 – Customer satisfaction with retail banks in Canada was high before the outbreak of COVID-19, but satisfaction is falling flat in the critical area of digital banking experiences, according to the J.D. Power 2020 Canada Retail Banking Satisfaction Study,SM released today. Overall satisfaction among banking customers in Canada has risen by five points to 790 (on a 1,000-point scale) from 2019, mainly driven by increases in score by the Big 5 banks. Overall satisfaction among midsize bank customers decreases two points to 796 from a year ago.

Alarmingly, while overall mobile banking usage increases this year to 63% from 55% a year ago, customer satisfaction with banks’ mobile offerings has declined significantly year over year to 828 from 832. The decline in mobile banking satisfaction occurs across all age and income groups, with the sharpest drops among Gen X1 customers (-10 points) and affluent customers (-10).

“Canadian banks have seen, for the most part, significant improvements in customer satisfaction related to products and fees, reasonableness of fees and problem resolution,” said John Cabell, director of banking and payments intelligence at J.D. Power. “At the same time, the massive investments made by banks in mobile offerings have yet to show dividends in terms of elevating customer satisfaction. As many more customers must now reluctantly rely heavily on remote access to banking services due to COVID-19, rapid improvements in online and mobile are critical for Canadian banks to grow their retail business.”

According to the study, 49% of customers in Canada rely heavily on online and mobile banking, with 33% being defined as digital-only customers who predominantly use mobile or the internet for their banking needs. Overall satisfaction is lowest (777) among this group of digital banking customers, compared with branch-dependent digital customers (799) and branch-only customers (783). The low satisfaction of digital-only customers should be an alert to banks as more customers favor digital interaction over use of branches.

The study also shows that customers’ financial outlooks correlate not only with satisfaction with their bank but also with the likelihood they will choose the bank for their next financial service need. Overall satisfaction among customers who have a positive personal outlook about their financial situation averages 867, while overall satisfaction among those who have a negative or neutral financial outlook averages 758. Furthermore, 78% of customers with a positive outlook say they plan to use their current bank the next time they need an account or financial product, compared with only 54% of customers with a negative or neutral outlook. With mounting concern regarding further economic hardship, this trend highlights a valuable opportunity for banks to better address the needs of increasingly anxious customers.

Following are additional key findings of the 2020 study:

- Digital pain points: Lack of information clarity and ease of navigating the mobile app are the key reasons for customers’ declining satisfaction with banking digital channels. Additionally, banking advice received via digital channels, such as email and mobile app, is trending upward, yet it only meets customer needs 51% of the time vs. advice received at the branch (67%) or via phone with a bank representative (59%).

- Big banks lead midsize banks on digital engagement: Canada’s Big 5 banks have a larger proportion of customers who are highly engaged digitally with their financial institution (50%), compared with 46% among midsize bank customers.

- Gen Y customers hold the key for future growth: Among Gen Y customers, satisfaction increases the most year over year in the factors of ABM (automated banking machine); products and fees; and communication and advice. Members of this group hold the key for retail banks’ future business growth as they tend to have a college or other advanced degree and are affluent or mass affluent, defined as having an annual income between CAD$90,000-CAD$175,000.

Study Rankings

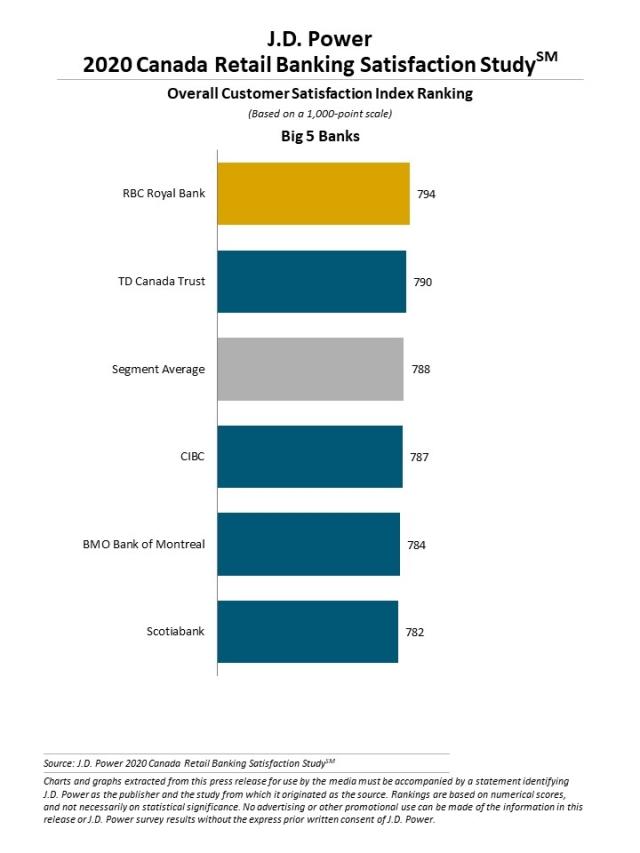

Among the Big 5 banks, RBC Royal Bank ranks highest with a score of 794. TD Canada Trust (790) ranks second. The segment average is 788.

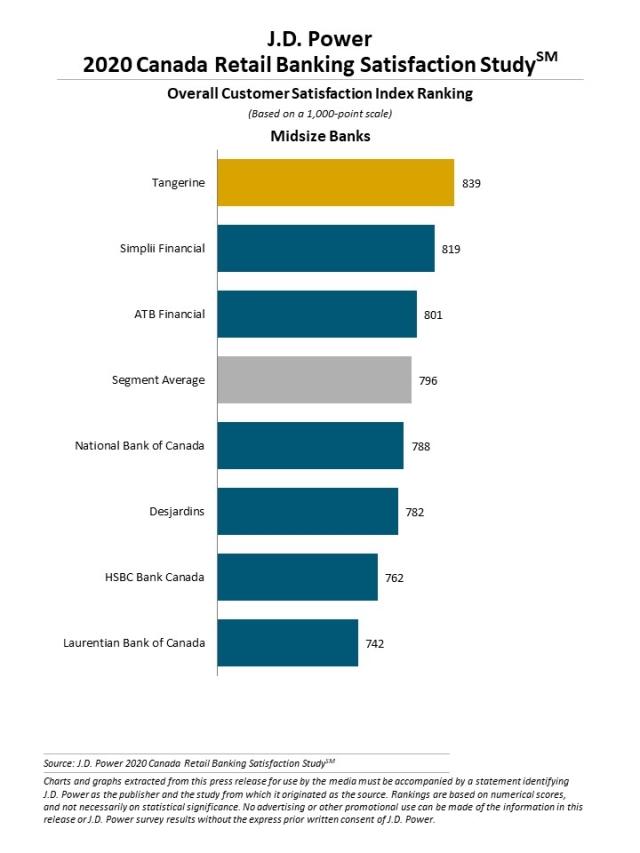

Among midsize banks, Tangerine ranks highest for a ninth consecutive year, with a score of 839. Simplii Financial (819) ranks second and ATB Financial (801) ranks third.

The Canada Retail Banking Satisfaction Study, now in its 15th year, measures customer satisfaction with Canada’s large and midsize banks. The scores reflect satisfaction among the entire retail banking customer pool of these banks, representing a broader group of customers than solely the branch-dependent and digital-centric segments.

The study measures customer satisfaction in six factors (listed in alphabetical order): channel activities; communication/advice; convenience; new account opening; problem resolution; and products/fees. Channel activities include seven sub-factors (listed in alphabetical order): assisted online service; ABM; branch service; call centre service; IVR/automated phone service; mobile banking; and online banking. The study is based on responses from nearly 14,000 retail banking customers of Canada’s largest and midsize banks regarding their experiences with their bank. It was fielded from July 2019 through January 2020.

For more information about the Canada Retail Banking Satisfaction Study, visit https://canada.jdpower.com/resource/canada-retail-banking-satisfaction-study.

J.D. Power is a global leader in consumer insights, advisory services and data and analytics. These capabilities enable J.D. Power to help its clients drive customer satisfaction, growth and profitability. Established in 1968, J.D. Power has offices serving North America, Asia Pacific and Europe.

Media Relations Contacts

Gal Wilder, Cohn & Wolfe; 647-259-3261; gal.wilder@cohnwolfe.ca

Madelyn Boelhouwer, Cohn & Wolfe, 647-259-3283; madelyn.boelhouwer@cohnwolfe.ca

Geno Effler, J.D. Power; Costa Mesa, Calif.; 714-621-6224; media.relations@jdpa.com

About J.D. Power and Advertising/Promotional Rules: http://www.jdpower.com/business/about-us/press-release-info

1J.D. Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2004). Millennials (1982-1994) are a subset of Gen Y.