Is Your Next Investment Advisor a Robo-Advisor?

National Bank Direct Brokerage Ranks Highest in Investor Satisfaction with Discount Brokerage Firms in Canada

TORONTO: 21 September 2015 —Discount brokerage firms need to deliver greater value to investors via tools that provide guidance such as automated portfolio management or “robo-advice.” While not yet widely adopted or even understood by investors, robo-advice has significant appeal, especially among Gen Y/Z[1] investors, according to the J.D. Power 2015 Canadian Discount Brokerage Investor Satisfaction StudySM released today.

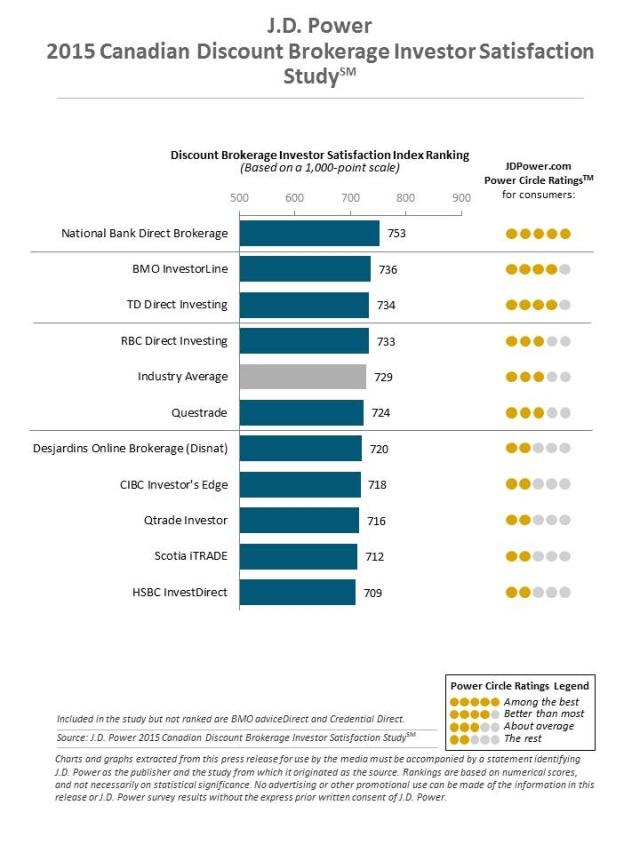

The study, now in its seventh year, measures investor satisfaction with their primary discount brokerage firm across six key factors (in order of importance): interaction; account information; trading charges and fees; product offerings; information resources; and problem resolution. Scores are calculated on a 1,000-point scale. Overall satisfaction with discount brokerage firms is 729, a 7-point decline from 2014.

For more information about the 2015 Canadian Discount Brokerage Investor Satisfaction Study, please visit http://canada.jdpower.com/resource/canadian-discount-brokerage-investor-satisfaction-study

Firms that perform well in overall investor satisfaction are not necessarily the lowest priced, but are firms that effectively develop “guidance-based” relationships with their clients. The key elements of those relationships include effective communications, useful digital tools and access to relevant educational resources. Satisfaction is 848 when investors are contacted two or more times by their firm about products and services, when they use at least one financial planning and one tracking/monitoring tool, and are aware of such educational resources as seminars/webinars. In contrast, satisfaction among investors for whom none of these are met is only 645.

For investors seeking more guidance and support but who do not want a traditional full service advisor, the robo-advisor may be a good fit. Robo-advisors provide automated portfolio management services, including periodic re-balancing, at a relatively low cost based on assets. Several firms offer such tools already, but there is still limited awareness of this capability among investors, with 22 percent indicating they are aware of its existence. However, 56 percent of investors indicate they would be interested if their firm provided it, and interest climbs to 67 percent among Gen Y/Z investors.

“Robo-advisors have created a lot of buzz in the industry and could really take hold, especially with Gen Y/Z investors, if firms can get the pricing right and effectively communicate the value to those investors looking for guidance but not interested in or willing to pay for a full service advisor,” said Mike Foy, director of the wealth management practice at J.D. Power. “It could also help take some market share from full service providers over time, especially as investors begin to get more insight into their account fees and portfolio performance as key milestones for the CRM2[2] regulatory mandate approach.”

KEY FINDINGS

- The relative importance of commissions and fees as a driver of satisfaction has decreased, as the average cost per trade has declined for a third consecutive year ($11.08 in 2015 from $13.44 in 2014). Differences in pricing have also decreased significantly in recent years, with the gap between reported fees for the highest- and lowest-performing firms in the study declining by nearly 50 percent since 2012.

- Firms need to do a better job of providing greater fee transparency. Just 35 percent of investors say they “completely” understand their fees, down from 42 percent in 2014. Satisfaction is significantly higher among investors whose firm has provided an explanation of fees than among those whose firm did not (765 vs. 678, respectively).

- Providing an outstanding discount brokerage investor experience generates high levels of retention, advocacy and investment levels, and firms should be proactive in efforts to increase satisfaction. The study finds that 68 percent of highly satisfied investors (overall satisfaction scores of 900 or higher) say they “definitely will not” switch firms; 74 percent say they “definitely will” recommend their firm; and 45 percent say they have increased the amount invested with their primary firm in the past 12 months. However, when firms are complacent and investors are less satisfied (overall satisfaction scores of 700-799), just 29 percent say they “definitely will not” switch firms; 18 percent say they “definitely will” recommend their firm; and 36 percent say they have increased the amount invested with their primary firm in the past 12 months.

- While website remains the primary point of interaction for investors, providing a seamless multi-channel experience drives satisfaction higher when adding touch points such as live phone (+25), investment centre (+33) or mobile (+41).

Discount brokerage investment firm rankings

National Bank Direct Brokerage ranks highest in discount brokerage investor satisfaction with a score of 753, and performs particularly well in the interaction, account information and product offerings factors. Following in the rankings are BMO InvestorLine (736); TD Direct Investing (734); and RBC Direct Investing (733).

The 2015 Canadian Discount Brokerage Investor Satisfaction Study includes responses from more than 2,700 investors who use investment services with discount brokerage firms in Canada. The study was fielded from May 4, 2015, through June 1, 2015.

Media Relations Contacts

Gal Wilder; Cohn & Wolfe; Toronto, Canada; 647-259-3261; gal.wilder@cohnwolfe.ca

Beth Daniher; Cohn & Wolfe; Toronto, Canada; 647-259-3279; beth.daniher@cohnwolfe.ca

John Tews; J.D. Power; MI, USA; Tel: +1-248- 580-6218; media.relations@jdpa.com

About J.D. Power and Advertising/Promotional Rules www.jdpower.com/about-us/press-release-info

About McGraw Hill Financial www.mhfi.com

[1] J.D. Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2004). For purposes of this analysis, Gen Y and Gen Z are combined, as respondents are required to be at least 18 years old to participate in the study.

[2] For information about The Client Relationship Model - Phase 2 (CRM2), go to https://www.osc.gov.on.ca/en/Dealers_crm2-faq-planning-tips.htm